Skip to main content

Hit enter to search or ESC to close

Close Search

search

Menu

Payroll Solutions

Mobile Bank Account

Resource Hub

Employer Resource Hub

Learning Resource Hub

Contact

Request Demo

Payroll Login

search

Payroll Solutions

Mobile Bank Account

Resource Hub

Employer Resource Hub

Learning Resource Hub

Contact

Request Demo

Payroll Login

© 2022 NOW Money. All rights reserved.

Tag

fintech

NOW Money blog

What it’s like launching a Fintech startup in the UAE

NOW Money blog

A technical insight on how to be certified to operate in the Payment Card Industry

NOW Money blog

Why FinTech and Banks need each other

NOW Money blog

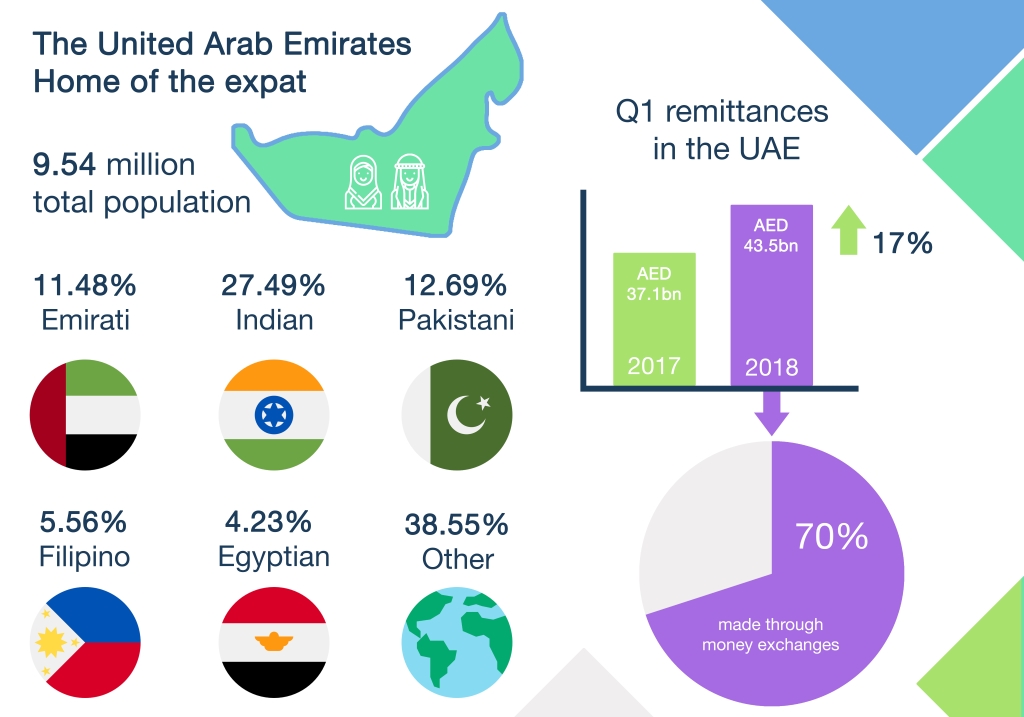

UAE – Home of the expat

NOW Money blog

A brighter future

Features

NOW Money blog

The poverty premium: It costs more, to be poor.

UAE Culture

A long way from home…

UAE Culture

Missing 10 years of your child’s life; is it worth it?

UAE Culture

Working 7am-7pm, what a way to make a living

Features

NOW Money blog

UAE VAT for FinTech companies explained

Features

NOW Money blog

4 reasons to meet us at RegTech MENA

Features

NOW Money blog

8 misconceptions about the UAE and its residents

1

2

3

Next